Thriving Through Tax Season: Galíndez LLC’s Commitment to Team Wellness

There is busy. Then, there are CPAs during tax season. This time can be incredibly......

03 April, 2024A collection of news and stories about our people, our capabilities, our research, and the ever-changing face of our firm. If you have a topic in mind you’d like to learn more about CONTACT US.

There is busy. Then, there are CPAs during tax season. This time can be incredibly......

03 April, 2024

As International Women’s Day approaches, Galíndez LLC takes a moment to reflect on the invaluable......

07 March, 2024

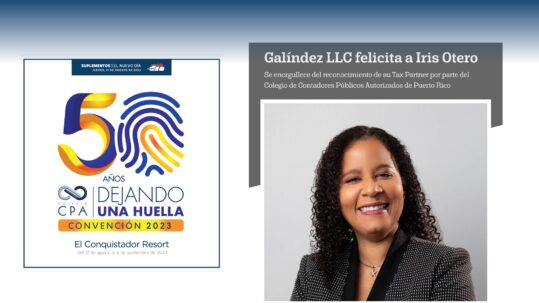

Galíndez LLC sprinted to the finish line at the 2024 Colegio de Contadores Públicos Asociados......

04 March, 2024

Galíndez LLC continues its commitment to education and professional development with its latest seminar aimed......

28 February, 2024

Galíndez LLC made a strong presence at the annual Health Industry Summit hosted by Industrials......

26 February, 2024

The Galíndez LLC team, led by Partner Kenneth Rivera and joined by Partner Iris Otero,......

21 February, 2024

Galíndez was thrilled to participate in the second edition of the Tax Bowl hosted by......

12 February, 2024

In the ever-evolving field of healthcare, consulting has become a vital component for organizations striving......

09 February, 2024

Galíndez, LLC recently hosted an insightful press conference to unveil its latest research study conducted......

09 February, 2024

Our tax department recently immersed in a full-day seminar at the Hyatt Place Hotel in......

31 January, 2024

Galíndez LLC kicked off the 2024 seminar series with its first in-house seminar at Chavales......

25 January, 2024

Galíndez LLC proudly announces significant leadership changes, effective January 1st, 2024. Rafael “Rafi” Nieves, CPA,......

27 December, 2023

Amidst the lush green hills of Naranjito, Galindez LLC recently hosted its annual holiday celebration......

26 December, 2023

At Galindez LLC, the holiday season is more than just a time of celebration; it’s......

22 December, 2023

The recently concluded 2023 PRASFAA Convention was a great success. It included a platform to......

13 December, 2023

Galindez LLC had the honor of having a representation at the 2023 PRASFAA Convention, commemorating......

11 December, 2023

At Galindez LLC, the spirit of Thanksgiving extends beyond a traditional meal—it’s a celebration of......

29 November, 2023

Last Wednesday, November 15, 2023, at the Puerto Rico Chapter of the HFMA event, Galindez......

17 November, 2023

In a demonstration of unwavering support for the fight against breast cancer, Galíndez LLC actively......

27 October, 2023

Galindez recently hosted a comprehensive full-day seminar at the Aloft Hotel in the Convention Center......

23 October, 2023

At Galindez LLC, we recognize that our most valuable asset is our dedicated team. Their......

09 October, 2023

At Galíndez LLC, we are proud that the honor of being recognized as CPA of......

01 September, 2023

Galíndez LLC proudly announces the debut of our very own basketball team. Joining a distinctive......

25 August, 2023

Galíndez LLC achieves yet another milestone with a highly successful in-house seminar! Geared primarily toward......

21 August, 2023

At Galindez LLC, we understand that a productive and enjoyable work environment is the cornerstone......

18 August, 2023

On July 20th, Galindez LLC had the immense pleasure of receiving the young and talented......

31 July, 2023

The CPA Youth Committee of the Puerto Rico Society of CPAs (CCPA) hosted an exciting......

05 June, 2023

The height of the tax season is a period of maximum productivity in a financial......

24 May, 2023

For the past few years, Galindez LLC has proudly been part of Nexia, a global......

10 May, 2023

Galindez LLC recently celebrated Administrative Professionals Day with an unforgettable event at Vin’us Bar and......

03 May, 2023

As we close out the fiery first quarter of the tax season, Galíndez LLC hosted......

19 April, 2023

The Galíndez LLC oversight treated their staff to a special COFFEE DAY with the visit......

29 March, 2023

El Nuevo Día recently reported on the condition of the healthcare industry on the island,......

27 February, 2023

On February 24, 2023, Galíndez LLC was present at the Puerto Rico Manufacturers Association 2023......

27 February, 2023

The College of Certified Public Accountants of Puerto Rico (CCAPR) held its first Tax Bowl......

10 February, 2023

On February 9th, 2023 Galindez LLC’s Tax Partners Kenneth Rivera and Levi Villegas will take......

08 February, 2023

Puerto Rico is known for being one of the most spirited celebrants of the holidays.......

19 December, 2022

Galíndez LLC’s team came together to learn and laugh for the annual Thanksgiving lunch. Celebrated......

29 November, 2022

On Saturday, November 12th, the Interamerican University of Puerto Rico, Ponce Campus, was host and......

14 November, 2022

October 9th marked another great memory for the Galíndez LLC team. As both participants and......

10 October, 2022

As firm advocates for community involvement and joining in the fight against breast cancer in......

15 September, 2022

It is with great pride that Galindez LLC announces that our own Leví Villegas, CPA,......

15 September, 2022

Galindez LLC’s professionals have contributed to a number of important tax and audit forums hosted......

01 July, 2022

With the busiest part of the 2022 tax season behind us, Galíndez LLC’s team took......

20 June, 2022

The Puerto Rico Chamber of Commerce (PRCC) is celebrating its 2022 annual convention with the......

10 June, 2022

Do you know about the revised due dates for the 2021 Tax Season? Your trusted......

14 April, 2022

Your trusted team of Tax Consultants at Galíndez LLC wishes to share some updated information. The Puerto Rico......

11 April, 2022

Galindez LLC’s commitment to excellence for all our clients, including the corporate and banking arena,......

07 April, 2022

As we quickly approach Tax Day 2022, Galíndez LLC’s own Tax Partner Leví Villegas shared......

07 April, 2022

On January 1st, 2022 our firm announced our new corporate identity: Galindez LLC. With much......

28 January, 2022

On January 1st, 2022 our firm announced its new corporate identity. With much excitement, we......

26 January, 2022

Your trusted team of Tax Consultants at Galíndez LLC wishes to share some updated information. The......

28 October, 2021

The debt adjustment plan for Puerto Rico has been a hot topic in the recent......

21 October, 2021

Every day, five women are diagnosed with breast cancer in Puerto Rico. 39 years ago......

26 July, 2021

Galíndez, LLC is a proud member of Nexia International, a global network of independent accounting......

12 March, 2021

As part of the Economic Pulse section of the monthly edition of their magazine Hospitales,......

18 December, 2020Through our international partnership, Galíndez, LLC, Together Business Consulting, and other Nexia International firms around......

25 November, 2020

There is no doubt that these are times of rapid changes in fluctuating global markets.......

20 November, 2020

As the year 2020 gets ever nearer to its conclusion, there is no doubt that......

19 October, 2020

Galindez, LLC Partner and Tax Expert Kenneth Rivera shares with El Nuevo Día readers his......

21 September, 2020

The Puerto Rico Treasury Department has recently announced new incentives for the private sector through......

17 September, 2020

November 2019 marked the start of an unprecedented international health phenomenon, with devastating economic and......

01 September, 2020

On August 8, 2020, President Trump signed a Presidential Memorandum (“the Memo”) authorizing employers to......

01 September, 2020

Galindez, LLC Partner and Tax Expert Kenneth Rivera shares with El Nuevo Día readers his......

10 June, 2020

Your trusted team of advisors at Galíndez, LLC wants to keep you informed about the......

06 June, 2020

Thanks to the incredible amount of clients we’ve had the honor of assisting, our team......

06 June, 2020

As the list of PPP recipients grows, so does the agencies’ need for auditing across......

06 June, 2020

With the new changes signed into law last Friday, June 5th, and the release issued......

06 June, 2020

If you need any help navigating these programs, your trusted team of advisors......

05 June, 2020

As stated by the Executive Order issued by the Governor of Puerto Rico, professional activities......

04 May, 2020

Your team of consultants at Galíndez, LLC is proud to provide up-to-date, practical information on......

27 April, 2020

As a result of Governor of Puerto Rico’s Executive Orders No. OE-2020-020 and OE 2020-023......

31 March, 2020

Anticipating potential problems that taxpayers and merchant may confront in the near future, as a......

31 March, 2020

On March 18, 2020, the Puerto Rico Treasury Department (“Treasury”) issued the Administrative Determination 20-08......

31 March, 2020

Due to the COVID-19 emergency, on March 18, 2020, the Puerto Rico Treasury Department (“Treasury”)......

30 March, 2020

As many of us have been made aware, COVID-19 may increase existing risks to your......

18 March, 2020

Considering the economic distress that COVID-19 impact might have in taxpayers, the Puerto Rico Treasury......

16 March, 2020

Pursuant to the Puerto Rico State Department portal, the due dates to file the 2019......

16 March, 2020

As of February 24, 2020, the Third Phase of SURI transition took place. As a......

16 March, 2020

As a result of Executive Order No. OE-2020-020 issued on March 12 by the Governor......

16 March, 2020

As experienced after Hurricane María, the PRTD issued Internal Revenue Circular Letter No. 20-08 (“CC......

14 March, 2020

Pursuant to Internal Revenue Circular Letter CC RI 20-09 (“the Letter”) eligible individuals can make......

14 March, 2020

On February 24, 2020, the PRTD completed the third phase of the transition to the......

14 March, 2020

Pursuant to the Internal Revenue Circular Letter 19-15, every taxpayer will be required to electronically......

14 March, 2020

INDIVIDUALS For 2019, the electronic filing of the income tax return (“return”) could be completed......

13 March, 2020

On December 30, 2019, the PRTD issued Internal Revenue Circular Letter 18-21, to notify the......

12 March, 2020

The PR Code was amended by Act No. 257 of 2018, to establish the requirement......

12 March, 2020

n response to a recent court case, the PRTD issued the Internal Revenue Circular Letter......

11 March, 2020

Act No. 257 was enacted on December 2018 and made substantial changes to the Puerto......

02 March, 2020

On January 8, 2020, the PRTD issued the Internal Revenue Circular Letter No. 20-02 (“Circular......

13 January, 2020

On January 9, 2020, the Puerto Rico Treasury Department (PRTD) issued the Administrative Determination 20-01......

11 January, 2020

The Galíndez, LLC team is proud to support the Association for Youth and Community of......

08 December, 2019

Galíndez, LLC was proud to be a part of United Way’s ‘Regala un Día’® (‘Give......

01 September, 2019

On August 2, 2019, the Puerto Rico Treasury Department (“PRTD”) issued Administrative Determination Number 19-03......

06 August, 2019

At Galíndez, LLC we’re all about team building and the great culture that sets us......

10 July, 2019

The PRTD issued the Internal Revenue Circular Letter Number 19-11 on May 17, 2019 to......

26 June, 2019

On December 10, 2018, Act 257 (“Act 257-2018”) was enacted to incorporate several amendments to......

23 June, 2019

Recognizing that a large number of taxpayers have not been able to obtain all the......

22 June, 2019

The Puerto Rico Treasury Department (“PRTD”) issued Internal Revenue Circular Letter Number 19-10 (“IRCC 19-10”)......

20 June, 2019

Another important partnership we have is with “Fondos Unidos de Puerto Rico”. For more than......

20 June, 2019

The 2017 Tax Cuts and Jobs Act (the “TCJA”) incorporated in the United States Internal......

16 June, 2019

A Special Announcement to all our Esteemed Clients: We are extremely excited to announce that......

15 June, 2019

On September the 21st, 2017, life for all Puerto Ricans was forever changed as Hurricane......

01 June, 2019

Social commitment is very important to Galíndez LLC, a core value we hold dearly. We......

01 June, 2019

Music is one of the most fabulous expressions of the human being because it manages......

26 May, 2019

Education is a significant part in a person’s life. Every day, a student is grappled......

15 May, 2019

At Galindez, LLC we are proud to support the community, foster corporate accountability and promote......

10 May, 2019

Galíndez, LLC is a proud supporter of our community, and on this occasion we are......

01 May, 2019

On December 10, 2018, the PRTD issued Administrative Determination Number 18-14, to simplify the rules......

22 February, 2019

The PRTD issued Internal Revenue Circular Letter Number 18-17 on December 7, 2018 to inform......

20 February, 2019

On January 29, 2019 the PRTD issued the Internal Revenue Informative Bulletin Number 19-02 to......

20 February, 2019

The PRTD issued Internal Revenue Informative Bulletin Number 18-24 to clarify certain tax amendments incorporated......

18 February, 2019

On December 4, 2018, the PRTD, issued Internal Revenue Circular Letter Number 18-15, to establish......

15 February, 2019

The PRTD issued Internal Revenue Circular Letter 18-20 (“IRCL 18-20”) on December 28, 2018, to......

15 February, 2019The PRTD issued Publication 06-06 on January 29, 2019, to notify taxpayers about the new......

04 February, 2019

The PRTD issued the Internal Revenue Circular Letter Number 19-01 on January 23, 2019, to......

03 February, 2019

Pursuant to Section 4041.03 of the PR Code, every merchant who is not a withholding......

01 February, 2019

On December 31, 2018, the PRTD issued Internal Revenue Circular Letter 18-21, to notify the......

01 February, 2019

* Certain requirements and conditions apply. Please see below for more information. ** Portal was supposed......

05 June, 2018

The Treasury Department (the “Department”) issued Administrative Determination No. 18-07 (the “Determination”). The Determination basically......

03 April, 2018

Treasury issued Administrative Determination 18-05 (“Determination”), which provides how individuals will claim any losses suffered......

05 March, 2018

On March 1, 2018, the Treasury issued Informative Bulletin 18-08 (“the Bulletin”) with the purpose......

02 March, 2018

On February 12, 2018, the Supreme Court of Puerto Rico published their most recent tax......

01 March, 2018

The Treasury issued on January 30, 2018, the Internal Revenue Circular Letter No. 18-01 to......

03 February, 2018

On January 30, 2018, the Puerto Rico Treasury Department (“Treasury”) issued Internal Revenue Informative Bulletins......

30 January, 2018